How to Avoid Making Investment Mistakes

FOR CLIENTS

Many people underestimate their investment time horizon, which makes their investment objectives be misaligned with their investment strategy.

If this is you, then take note: these investment mistakes add up and can reduce the value of your retirement nest egg.

In this blog, my goal is to help you identify common investing mistakes and learn how to avoid them.

Underestimating your investment time horizon

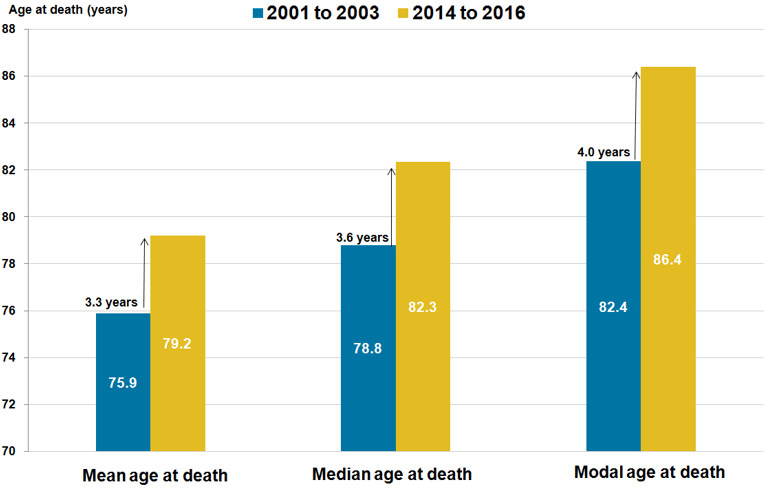

How long do you believe you will live? How long do you expect your spouse to live? Typically, investors overestimate the length of their lives, which can be problematic when planning their financial futures.

Medical breakthroughs happen all the time. As medical treatment, diets, and living standards improve, many people are living longer lives than they expected. As the population ages and life expectancy increases, so do the costs of healthcare and living longer.

Many people underestimate their own life expectancy. As a result, they do not make financial plans for a longer life and they run the risk of depleting their savings before they die.

It is therefore critical to have a a sound financial plan in place, that aims to provide financial stability throughout retirement. A sound financial plan is also essential for those who want to increase the value of their assets, in order to leave a legacy to loved ones and family members who survive them - which makes the investment time horizon greater than their own.

In any case, making reasonable life expectancy time horizon assumptions is critical to your financial plan.

Amyr Rocha Lima, CFP® is a financial planner who specialises in working with successful professionals age 50+ to help them reduce taxes, invest smarter and retire on their terms.

SOURCE: Health state life expectancies, UK: 2014 to 2016

Misaligning your investment goals and investment strategy

Aligning your investment strategy with your investment goals is critical to long-term investing success.

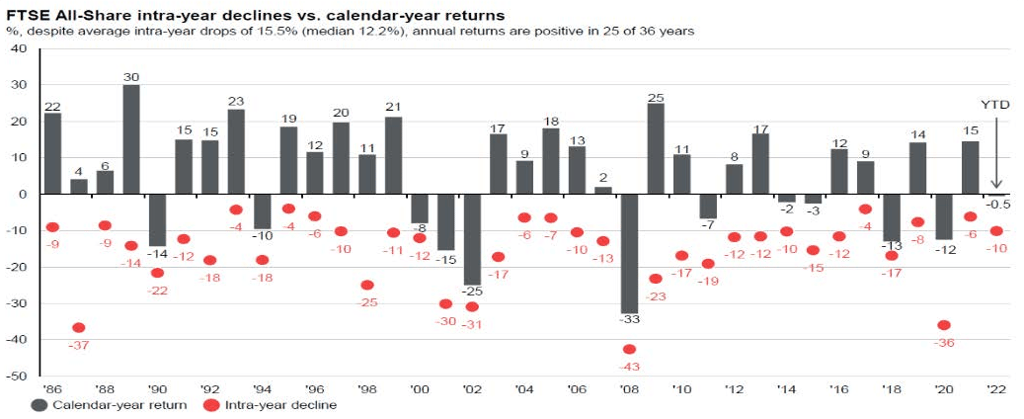

This may seem obvious, but many investors behave in a way that works against their goals. For example, conflating risk and volatility is a common mistake made by many investors.

In general, the longer the investment time horizon, the more volatility you can accept, and the less risk there is that volatility will work against you. Many investors, however, cannot withstand the volatility required to achieve their investment objectives. They are more concerned with short-term volatility than with the long-term likelihood of achieving their goals. As a result, their investment portfolio tends to underperform against their objectives.

SOURCE: JPMorgan Guide To Retirement 2022

Some investors, for example, consistently load their investment portfolios with cash and bonds, fearing that stocks will fall in the short term.

But cash and bonds frequently produce returns that are barely above the rate of inflation. This in turn reduces the likelihood of achieving a longer-term goal of real growth above inflation, especially if withdrawals are also anticipated.

Those with shorter investment time horizon objectives, on the other hand, are frequently overly exposed to volatility, increasing the risk of loss that could jeopardise their entire financial future.

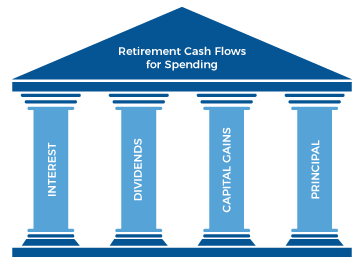

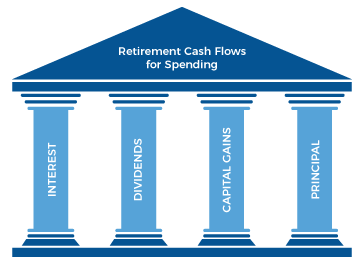

Misaligning your income needs with your cash flow needs

Income and cash flow are not the same thing, and many investors get them mixed up. In fact, the two distinct concepts, as well as the distinctions between them, are critical.

Simply put, cash flow is the amount of money required for living expenses and other personal needs. Income, on the other hand, is the amount of dividends and interest earned by an investment portfolio, on which you will pay current income tax if it is a taxable account.

The key distinction is that how you generate income can have a tangible impact on the growth of your assets as well as the tax you pay, both of which impact your ability to achieve required cash flows.

It's a mistake to believe that you can get all of your cash flow from income and never touch capital. This notion, however, is difficult to overcome for many people. The emphasis should instead be on the total after-tax return.

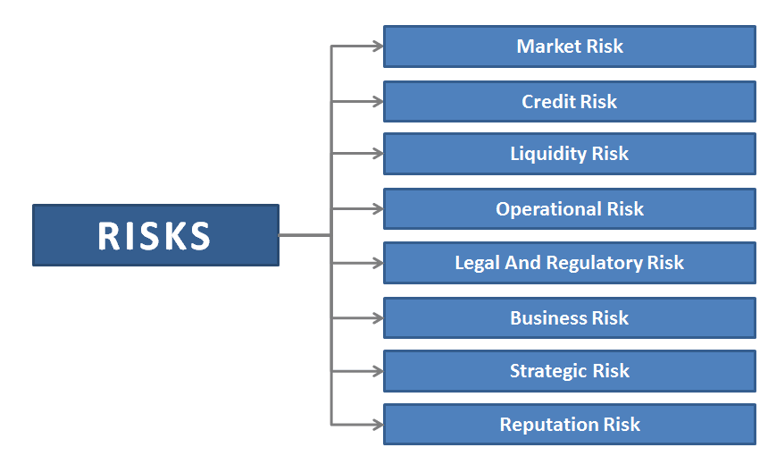

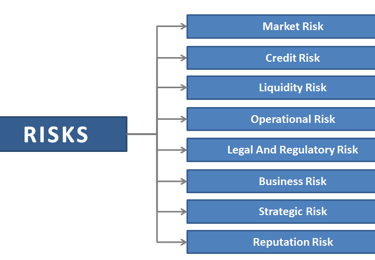

Ignoring unwanted risk factors

Investors may be unaware that managing a globally-diversified investment portfolio come with hidden risks. Indeed, DIY investment portfolios in particular are frequently overexposed to risk factors that were never properly identified. Do not allow this to happen to you.

A lot of excess risk results from unintended portfolio concentration. This exposes an investment portfolio to greater volatility and the risk of accelerated losses.

Factors such as sector, country, currency, valuations and size all play a role in a properly diversified portfolio. Furthermore, some assets are highly correlated with changes in interest rates or commodity prices.

Assume, for example, that you own one Japanese stock and one British stock. These may appear unrelated; however, consider each company's revenue source. Are they both susceptible to changes in interest rates? Is the performance of each linked to currency movements in a similar way?

A concentration of any of these factors, and others, in excess, can expose your portfolio to risks you did not intend.

SOURCE: Michael Kitces, www.kitces.com

SOURCE: CFA® Study Book

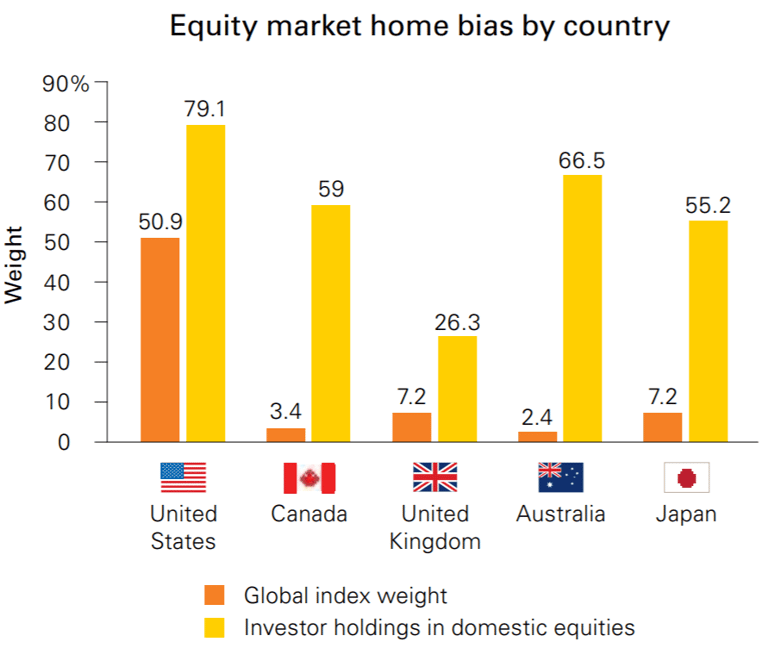

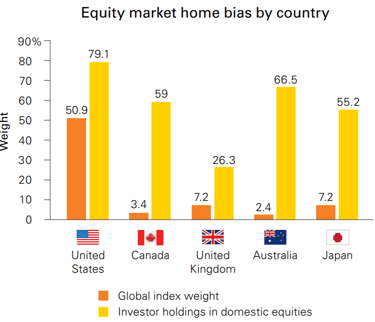

Ignoring global stock markets

As a result of globalisation, there are numerous innovative companies and investment opportunities developing around the world.

Therefore, don't make the mistake of focusing only on the UK stock market, because it feels "familiar". It is a mistake to believe that a portfolio is properly diversified simply because you have chosen stocks from various sectors. That is not sufficient.

Investment returns can be affected by the country's overall economic performance and political climate. A weak domestic economy makes it difficult for many businesses to thrive, so your investment portfolio might incur additional risks if you do not consider various countries and regions.

Many investors have a "home country bias" in their investment portfolio, which means they over-expose their portfolio to the country where they live. If, for example, you were to buy stocks diversified across all sectors in the United Kingdom, performance might be determined more by the UK's economic performance than by the performance of the chosen companies.

Diversification is an important component of constructing an investment portfolio. Investing abroad can help you strengthen your portfolio by expanding the pool of potential investments from which to choose.

SOURCE: Vanguard, based on data from the IMF's Coordinated Portfolio Investment Survey

Ignoring the Basic Importance of Supply and Demand

The fundamentals of supply and demand are easy to overlook.

Analysts and pundits cite an infinite number of theories about the mechanisms that drive stock prices. The simple fact remains, however: the supply and demand for stocks will always be the primary driver of share prices.

According to basic economic theory, the relative supply and demand for goods in an open market determines their prices. For example, if supply is equal, demand for ski equipment rises during the winter months, and thus the price of skis rises. During the summer, when people ski less, demand falls and prices fall.

Stock prices are no exception: they fluctuate based on short-term demand.

Because it takes time for companies to create new issues of stock, the supply of equities is relatively fixed in the short run. As a result, short-term price changes in markets are primarily caused by changes in demand. However, supply has the ability to change almost infinitely in the long run. As a result, supply becomes the dominant factor in stock prices over longer time periods.

Understanding the relationship between the supply and demand for stocks is critical when deciding whether or not to invest in stocks, because it empowers you to filter out irrelevant noise.

Making investment decisions based solely on publicly available information

What sources of information do most investors consult when making an investment decision?

With the possible exception of a 'hot tip' picked up at a dinner party, the information is likely to come from publicly-available sources, which can be a problem.

All publicly known information is efficiently discounted by stock markets. This means that as soon as a piece of information becomes available to the public, the share price reflects it. It makes no difference whether the information comes from the morning newspaper, research from your broker, radio, television, or the internet, or any other publicly-available source.

Despite this, many investors continue to speculate on this type of information.

To generate excess returns, you must either identify information that is not widely known, or interpret publicly-available information differently — and correctly — than the crowd. In other words, you must have knowledge that is not already reflected in stock prices. But this can lead you to...

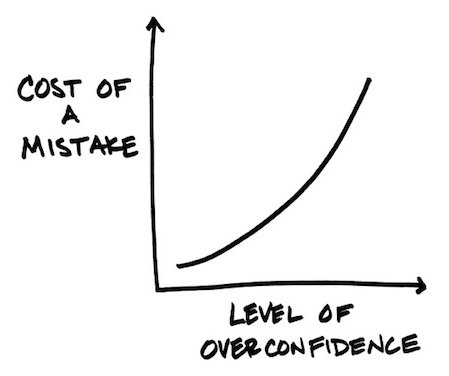

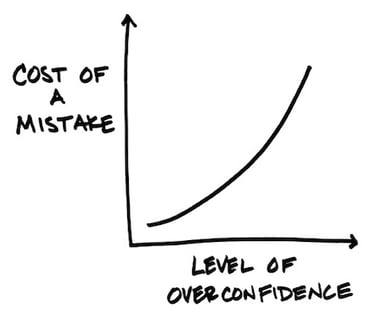

Being overconfident in your investing skills

When investing personal assets, it's natural to feel emotional ups and downs as you observe the daily ups and downs of stock markets.

You are, after all, dealing with your financial future. As a result, a slew of cognitive biases enter the picture, which can cloud your judgement and impede your ability to make rational, impartial decisions.

Let's face it: the human brain was not designed to invest! Our Stone Age forefathers evolved and survived by focusing on whatever assisted them in hunting and gathering food. Their biases shaped their beliefs, creating and reinforcing their worldview. And some of the core functions in our brains still see the world through this screen, as did our forefathers.

Many investors, for example, will focus on their successes while attempting to forget their mistakes, confirming their personal views rather than maintaining objectivity. This constructs a barrier that allow them to forget their past mistakes.

This tendency to focus on your successful investments can lead to overconfidence, which may result in you taking on unwanted risks. These biases affect everyone. That is why it is critical to create an environment for investing that is free of emotion, relying on data and objective analysis to make the best decisions for your financial future.

SOURCE: Behavior Gap

SOURCE: Wyckoff Price Cycle

Paying Excessive Fees

Private investors' returns are frequently harmed by the fees they pay.

Constantly tinkering with an investment portfolio can result in very high percentage annual charges. Even with today's "low cost" internet trading accounts, these fees can mean the difference between outperforming and underperforming against your investment objectives.

This can happen in a variety of ways. For example, if an investor self-manages a portfolio through a "low cost" broker, they will typically pay a set fee per trade as well as an annual administration fee. Therefore, unless the amount traded is relatively large, the set fee can be a surprising high percentage figure. This is referred to as a "trading fee." Given that DIY investors are known to engage in a high level of trading activity, the addition of a trading fee can be extremely detrimental to subsequent performance.

Investors who prefer not to self-manage can hire an independent financial adviser to build an investment portfolio, but this can cost 3% or more per year when adviser fees, underlying fund management fees, and portfolio turnover costs are factored in.

Therefore, to understand the true motivations of service providers, whether stockbrokers, financial advisers, fund management companies, or trading platforms, it is always necessary to determine how they derive their fees. The financial incentives for your financial adviser should be closely aligned with your own.

Have You Made Any of These Mistakes?

Nobody is perfect. We will all have our ups and downs, especially when it comes to investing. However, some of the mistakes you may make when investing are fairly common and are not limited to you alone. In fact, the vast majority of investors commit many of the mistakes stated above.

Even the most experienced investors find it difficult to avoid all investment pitfalls. The truth is that many investors simply do not have the time to sort through the vast amount of information available today and apply it to their unique, complex requirements.

”Amyr is patient, level headed and an expert financial planner. He has helped us work through our many questions to find sensible answers and to build a financial plan that is realistic, balanced and achievable. I would recommend him to anyone seeking advice on planning their financial future.”

David Claridge

(CEO - Dragonfly)

*****

”Amyr has helped my husband and I hugely as we began our journey of financial planning for our future. He has fantastic knowledge of the big tech corporate landscape and was able to help us uncover some great opportunities for investment, as well as helping us plan for our family's future and for early retirement.”

Emma Lancelotte

(Engagement Manager - Google)

*****

”Amyr did a great job helping us figure out our financial goals and the route to getting there. He was always very clear, available for follow ups or clarifications where needed and left us feeling in control of our finances.”

Ben Freeman

(Product Manager - Facebook)

*****

Here's what clients say

Let's chat

Ready to start building your financial plan?

Then you can book a free, no obligation call with me.

We'll have an initial conversation to better understand your requirements and to see whether my services would be a good fit.

Full Disclosure: Nothing on this site should ever be considered to be advice, research or an invitation to buy or sell any financial products.

Copyright © 2026, Amyr Rocha Lima

Free Guide

Let's Connect

Chartered Financial Planner | Kingston upon Thames